SAFE Notes, Convertible Instruments, and Pre-Revenue Startups in Divorce

Valuing a profitable company with years of earnings is hard enough. Valuing a pre-revenue startup is a different kind of problem. There may be no profits to capitalize, no comparable sales, and a last financing round whose implied valuation everyone privately knows is aspirational. Yet that equity still has to be characterized and accounted for in a Texas divorce. This page covers how courts and experts approach startup equity and the instruments that come with it.

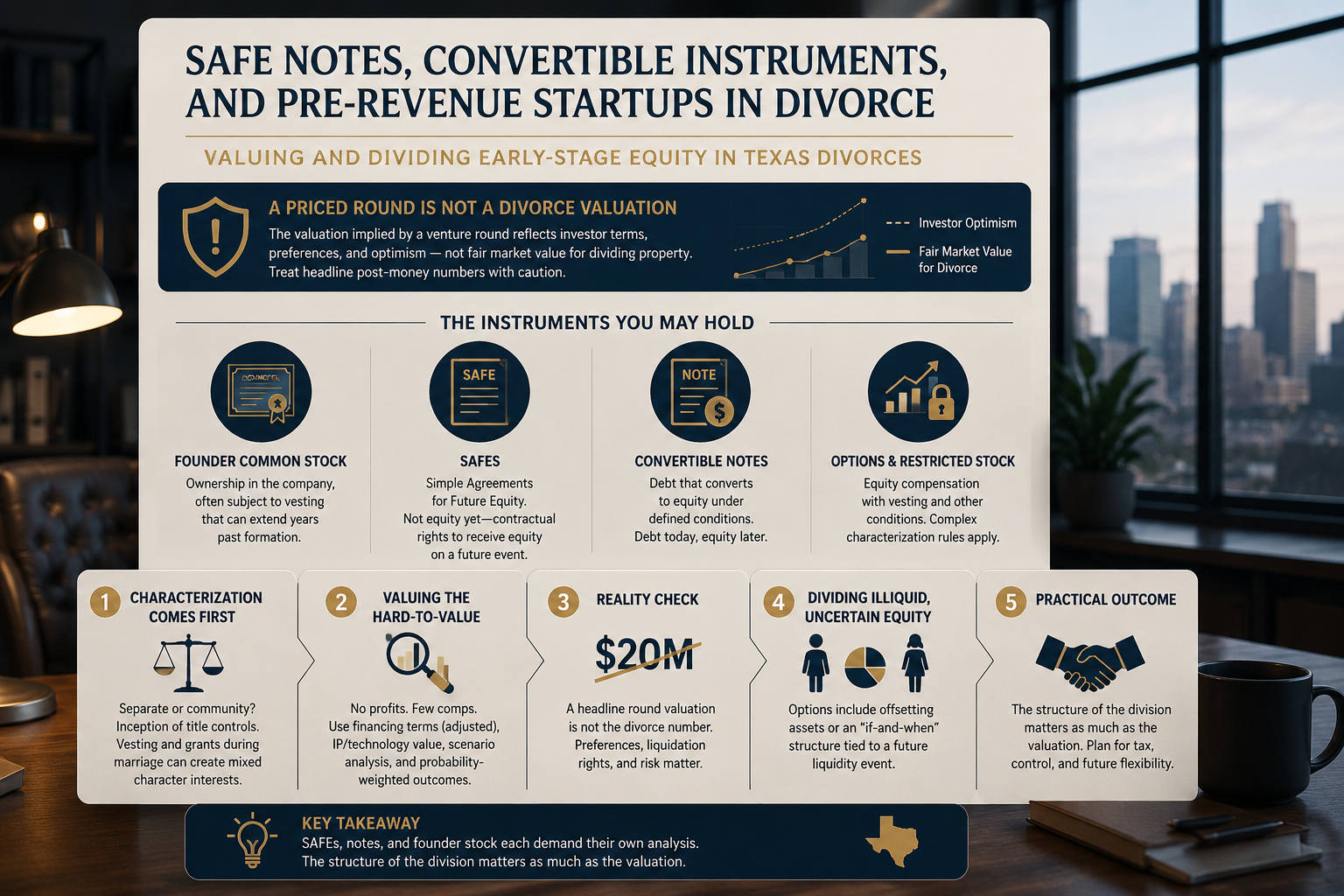

A priced round is not a divorce valuation

The valuation implied by a venture round reflects investor terms, preferences, and optimism — not fair market value for dividing property. Treat headline post-money numbers with caution; the real analysis is more careful.

The Instruments You May Hold

Startup wealth rarely looks like a simple stock certificate. Common forms include:

- Founder common stock, often subject to vesting that can extend years past formation.

- SAFEs (Simple Agreements for Future Equity), which are not equity yet — they are contractual rights to receive equity on a future triggering event, typically a priced round.

- Convertible notes, debt that converts to equity under defined conditions.

- Stock options and restricted stock, covered in depth in our stock options and RSUs page.

Each has a different legal nature, which affects both how it is characterized and how it is valued. A SAFE is a contract right, not stock; a convertible note is a debt instrument until it converts. Treating them all as “equity” is a common and costly oversimplification.

Characterization Comes First

As with any business interest, the threshold question is whether the equity is separate or community property, governed by the inception-of-title analysis. Founder stock issued before marriage is presumptively separate; equity or instruments acquired during marriage are presumptively community. Vesting complicates this: A grant made before marriage that vests during it, or made during marriage that vests after, can be mixed in character, which is the same apportionment problem the stock options page addresses in detail.

Valuing the Hard-to-Value

For a pre-revenue or early-stage company, the standard valuation approaches strain. Experts may turn to recent financing terms (adjusted for their distortions), the value of the technology or intellectual property, comparable early-stage transactions, or methods that probability-weight a range of future outcomes. Liquidation preferences and the rights of preferred investors mean common stock — what a founder usually holds — is often worth far less per share than preferred, a point headline valuations obscure.

In our experience, early-stage equity carries a wide range of defensible values, and the uncertainty is real rather than manufactured. This uncertainty argues for creative division structures rather than fighting to the death over a single number.

Dividing Illiquid, Uncertain Equity

Because startup equity is illiquid and its value uncertain, dividing it presents practical problems explored further on the dividing the business page. Options range from awarding the founder the equity and offsetting with other assets, to an “if-and-when” approach that divides proceeds only when a liquidity event occurs. Each has tax and control consequences, and an if-and-when structure keeps the parties financially entangled until exit, which is not ideal but is sometimes unavoidable when there is no cash to fund a clean buyout today.

Frequently Asked Questions

Equity in an early-stage company?

SAFEs, notes, and founder stock each demand their own analysis. The structure of the division matters as much as the valuation. Let’s map it out.

This page provides general information about Texas law and is not legal advice for your specific situation. Reading it does not create an attorney-client relationship.